- Over to You, Ms Lagarde …

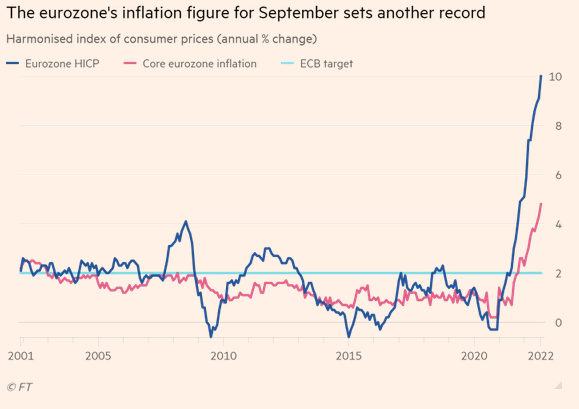

The Eurozone reported the highest inflation of 10% (annualized) this month, rising for the 11th time in a row and up from 9.1% in August. The prices of food, alcohol and tobacco rose by 11.8%. The core inflation rose by 4.8%. Dr. Doom (Nouriel Roubini) of NYU said, “the eurozone is heading for a ‘stagflationary hard landing’ caused by persistently high inflation and stagnant growth.” The problem for Europe and for other markets is that a tight labor market (as we saw the unemployment claims yesterday) will keep wages high and that will keep upward pressure on services prices as per Jessica Hinds of Capital Economics.

This reading will increase the pressure on the ECB to raise rates - higher and faster (75 or 100bps). The FT says, “the EU energy ministers are discussing windfall levies on non-gas power generators and fossil fuel companies and a cut to peak energy consumption of 5%, as well a potential cap on wholesale energy prices”. The impact of these measures would ‘soften the recession in the eurozone and lower the pace of inflation, but also mean the fall in inflation next year will be less accentuated b/c you will have stronger demand’, says Crsten Brzeski, an economist at ING. As we said earlier this week, Germany will be spending 200B euros on capping gas and electricity prices. This will lower next year’s inflation by three percentage points and soften the recession (the output will now decline vy 2 percent v. 3.5 percent) as Deutsche Bank’s economists.

- Chinese Service Sector …

Data from China’s National Bureau of Statistics indicated that the manufacturing activity returned to expansionary territory mainly b/c the power crunch is largely behind and government support measures are beginning to have an effect. But the services sector fell into contraction territory (from 51.9 to 48.9) and that pulled down the non-manufacturing index from 52.6 to 50.6. Beijing is dealing with high youth unemployment, slow income growth and ailing real-estate market.

As per China watchers, the Covid restrictions will remain in place for the rest of the year and that means this economic picture will remain weak. “We think the economy will continue to struggle over the coming months,” Zichun Huang of Capital Economics. The cities under the covid restrictions today account for 25% of the GDP, down from 28% - so the picture is improving. The property sector is key to China’s growth but its outlook remains cloudy. “The recent property easing policies didn’t seem to be making much difference,” said Rosalea Yao of Gavekal Dragonomics. “There is no indication the new policies are having a significant impact on sales.”

Corporate Corner:

- Nike (-10%) reported a 44% increase in inventory (people are not buying the swoosh as much as before) and will offer more discounts. It did register higher profits and revs in the latest quarter.

- Micron Technology (+1.5%) reported higher profits but there on everything was downhill - lower revenue, lower guidance and weaker demand

- Amylyx Pharma (+9.3%) is up after the FDA approved its ALS drug which slows the progression of the disease and extends survival.

- Rent-A-Center (-18.1%), the rent-to-own retailer cuts its current-quarter earnings guidance

- Blue Apron (+2.7%) told the street that its is CFO will leave the firm

- Generac (+1.6%), the backup generator firm, was rated as outperform by Cowen as the sell-side firm initiated coverage.

- Voya Financial (+1.2%) was upgraded by Piper Sandler to overweight.

Data Check:

Eurozone inflation came in at 10% outpacing the expected 9.7% number.

PCE

Headlines (exp. +0.3%) came in on the nose

Core (exp. +0.5%) rose by 0.6% or 4.9% (YoY v. 4.7%) - higher than expected - something that will worry the Fed.

Personal income (exp. +0.3%) rose by 0.3%

Personal spending (exp. +0.2%) rose by 0.4% - nobody is listening to the Fed (to curb spending)

Trading Desk:

Equities: The stock futures are up slightly - Dow +30, S&P +8, Nas +20, and VIX -0.41 (31.44). The European shares are up - FTSE +6bps, DAX +67bps, CAC +69bps, AEX +49bps, and STOXX +34bps. Asian shares closed mixed. HK +33bps, Nikkei -1.83%, ASX -1.23%, Mumbai +1.8% and Shanghai -55bps.

Commodities: The WTI -62bps, Brent +12bps, gold +35bps, and copper +22bps.

Currencies: The DXY index +13bps, euro -68bsp, yen down 4bps, pound -49bps, and AUD -31bps. Bitcoin -53bps ($19.3k).

Bonds: The US10y yields are down 3.5bps (3.716%), gilts -9bps (4.048%), and bunds -11.6bps (2.093%).